What was the difference between pre-1980 and post-1980?

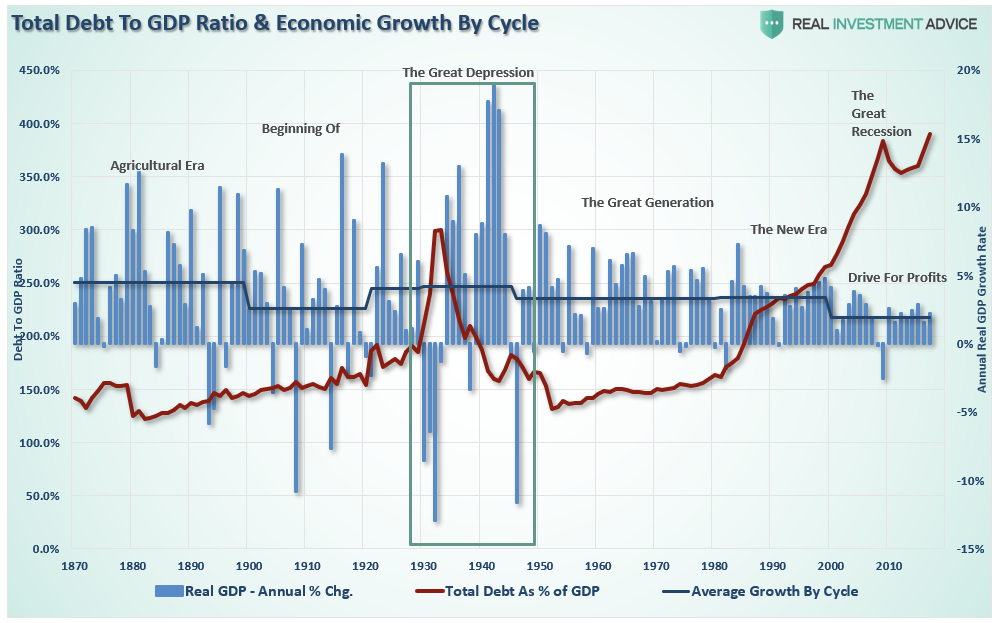

From 1950-1980, the economy grew at an annualized rate of 7.70%. This was accomplished with a total credit market debt to GDP ratio of less 160%. The CRITICAL factor to note is that economic growth was trending higher during this span going from roughly 5% to a peak of nearly 15%. There were a couple of reasons for this. First, lower levels of debt allowed for personal savings to remain robust which fueled productive investment in the economy. Secondly, the economy was focused primarily on production and manufacturing which has a high multiplier effect on the economy. This feat of growth also occurred in the face of steadily rising interest rates which peaked with economic expansion in 1980.

The obvious problem is the ongoing decline in economic growth over the past 35 years has kept the average American struggling to maintain their standard of living. As real wage growth remains primarily stagnate, consumers are forced to turn to credit to fill the gap in maintaining their current standard of living. However, as more leverage is taken on, the more dollars are diverted from consumption to debt service thereby weighing on stronger rates of economic growth. I have shown this gap previously.

Debt Doesn’t Create Real Growth

The massive indulgence in debt has simply created a “credit-induced boom” which has now reached its inevitable conclusion. While the Federal Reserve believed that creating a “wealth effect” by suppressing interest rates to allow cheaper debt creation would repair the economic ills of the “Great Recession,” it only succeeded in creating an even bigger “debt bubble” a decade later.

This unsustainable credit-sourced boom led to artificially stimulated borrowing which pushed money into diminishing investment opportunities and widespread mal-investments. In 2007, we clearly saw it play out “real-time” in everything from sub-prime mortgages to derivative instruments which were only for the purpose of milking the system of every potential penny regardless of the apparent underlying risk. Today, we see it again in accelerated stock buybacks, low-quality debt issuance, debt-funded dividends, and speculative investments.

When credit creation can no longer be sustained, the markets must clear the excesses before the next cycle can begin. It is only then, and must be allowed to happen, can resources be reallocated back towards more efficient uses. This is why all the efforts of Keynesian policies to stimulate growth in the economy have ultimately failed. Those fiscal and monetary policies, from TARP and QE, to tax cuts, only delay the clearing process. Ultimately, that delay only deepens the process when it begins.

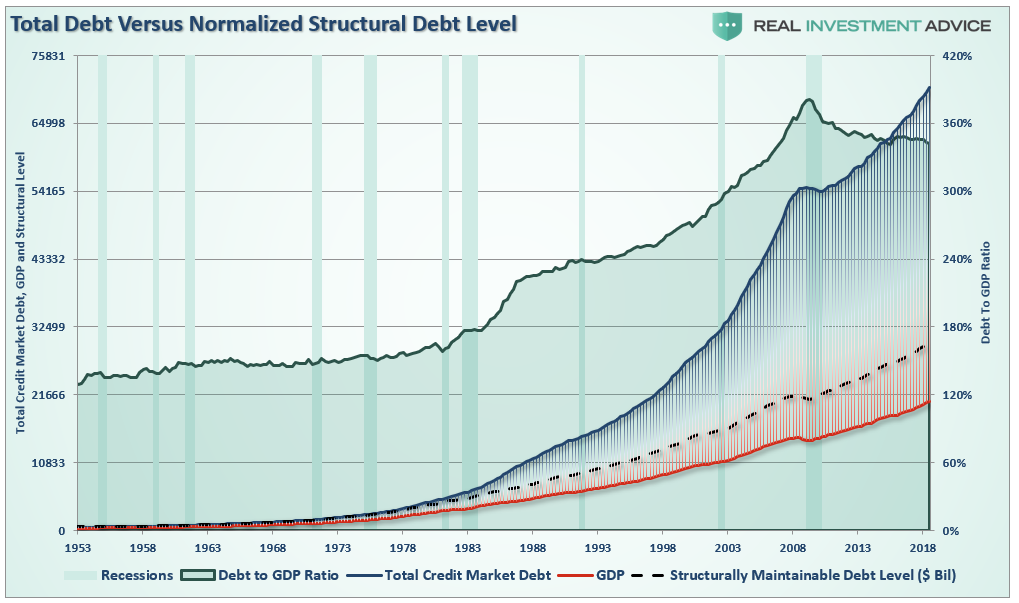

The biggest risk in the coming recession is the potential depth of that clearing process. With the economy currently requiring roughly $3 of debt to create $1 of economic growth. A reversion to a structurally manageable level of debt would involve a nearly $40 Trillion reduction of total credit market debt from current levels.

The economic drag from such a reduction would be a devastating process which is why Central Banks worldwide are terrified of such a reversion. In fact, the last time such a reversion occurred the period was known as the “Great Depression.”

This is one of the primary reasons why economic growth will continue to run at lower levels going into the future. We will witness an economy plagued by more frequent recessionary spats, lower equity market returns, and a stagflationary environment as wages remain suppressed while costs of living rise.

Debt – Is it just “correlation,” or is it “causation?”

You decide.

But one thing we know for sure is that “debt matters.”