I recently wrote an article discussing potential non-agency mortgage REIT risk on the horizon. Several non-agency mREITs have now continued to perform poorly, further diverging from agency mREITs. This difference appears to highlight a significant expectation that real estate will sustain a second move downward in the near-term.

The primary specific risk appears to be within non-agency mortgages. Without an agency backing, defaulting mortgages end up providing no payments and a considerably reduced value. Also, the underlying equity may not provide sufficient funds to satisfy the present value. Some non-agency paper is already priced to assume significant default likelihood upon a rate increase and/or continued depreciating prices.

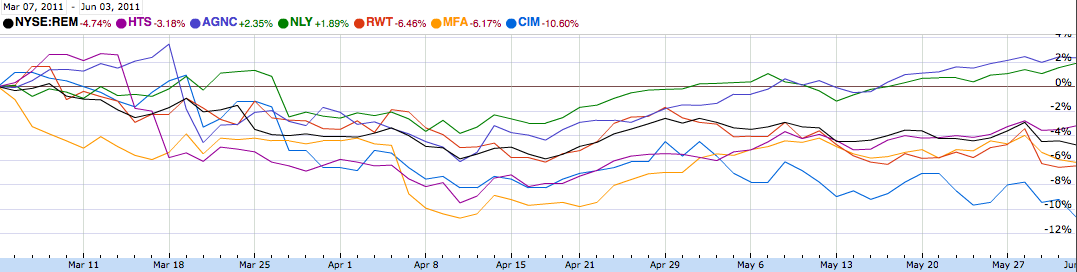

Three well-known non-agency mREITs are Chimera Investment Management (CIM), MFA Financial (MFA) and Redwood Trust (RWT), though these companies also can and do buy large positions in agency paper. These non-agency REITs have performed poorly in the short term on little to no news, and this performance appears to indicate increased market concern over this risk.

Their five-day chart:

[Click all to enlarge]

This poor performance appears over concerns that real estate will sustain a second move downward in the near-term. In contrast, agency paper has appreciated.

This poor performance appears over concerns that real estate will sustain a second move downward in the near-term. In contrast, agency paper has appreciated.

Agency mREITs & Spread Risk

Another risk is borne by the agency mortgage market. Agency mortgages are considered virtually risk-free, because U.S. agencies have guaranteed to step in and make payments to the lender on behalf of the non-paying borrower that they backed. These agencies can also choose to buy out the mortgage, and they often do exactly that after a borrower’s continued default for several months.

Three well-known agency mREITs are Annaly Capital Management, Inc (NLY), American Capital Agency Corp (AGNC) and Hatteras Financial Corp (HTS). There is always a minor risk that this whole market may become altered by future regulations to and/or agency interaction in mortgages, but such would likely only apply to future paper and not alter already existing guarantees.

An issue to several of the mREITs is the risk that interest rate changes will reduce future spreads. The market anticipates interest rate increases in the coming quarters and/or years, and another large wave of adjustable rate mortgages (ARMs) are scheduled to reset in 2012. Higher rates are generally expected to lower mREIT spreads. The performance of agency mREITs, which presently use high leverage to multiply this spread, indicates little market concern over dramatic spread changes.

Recent Market Activity Shows Increased Preference for Agency Paper

The past year was a relatively stable year for most mREITS, with most paying high dividends and also showing mild appreciation. Over the past quarter, of those named above, agency mREITs’ shares notably outperformed non-agency mREITs.

A three-month chart:

This divergence in performance should not be terribly unexpected. U.S. property values continue to depreciate and coming defaults and foreclosures appear increasingly likely. At some point, long term buyers may find discounted mortgage paper an attractive investment. Some non-agency paper and mREITS now offer yields in the double digits, which is abnormally high even for junk bonds. Exposure to non-agency mREITs should be limited to a reasonable percentage of a portfolio.

Higher income home owners with mortgages that are not guaranteed, such as jumbo mortgages, might be less likely to use bankruptcy as a backstop, because they have more to lose.

A good cautionary follow-up after the last article which also cautioned against the non-agency REITS.

I recently had to analyze for a client a portfolio of Freddie and Fannie inverse floaters. The fact that they were Freddie and Fannie issues meant that they were A-rated and found their way into a (now insolvent) insurance company's investment portfolio. I know absolutely nothing about how these securities were supposed to work, but I discovered that each pool of mortgages is sliced into dozens of tranches with different expected pay-back ratios and rates, and different interest rates attached to each different slice. It seemed to me that there was a greater early pay-back risk with some of them, and I'm assuming that defaults paid off by Fannie or Freddie are going to behave like CDs from insolvent banks that are paid off early -- although you get the principal, you lose the income stream and you lose the expected interest payments.

I'm really not a specialist in this area but I do own NLY. I suspect (but I don't know) that unanticipated early payoffs on defaults (and on restructures) may ultimately affect the income stream of even the agency REITS.

Regarding the non-Agency REIT's as plays on discounted paper: positively, value is there, but will still be there at lower prices before September, I feel.

The biggest problem we have are not with Bank of America mortgages or Chase or Wells or Citi, it's with government-owned mortgages: FHA, Fannie Mae, Freddie Mac. So the mortgages that the government controls, those should be the ones that we can modify the easiest. They should stop the foreclosures and they should say that these bankers can never foreclose on somebody unless every effort was made to modify that mortgage and that was documented.

from:

marketplace.publicradi.../

So please take it off this list!!!

Three stocks were down at the end of trading on Thursday.

CC Media Holdings’ posted an 8.33 percent stock gain to close at $6.50, to make it the leading local stock. CC Media Holdings owns global media and entertainment company Clear Channel Communications Inc.

The Dow Jones Industrial Average surged 75 points, or 0.63 percent, to close at 12,049.

Thursday’s closing tally:

• Abraxas Petroleum Corp. (NASDAQ: AXAS) — $3.78, up 4.42 percent, 52-week low/high ($2.27 - $6.16).

• Alamo Group Inc. (NYSE: ALG) — $22.21, down 3.31 percent, 52-week low/high ($18.68 - $29.27).

• Biglari Holdings Inc. (NYSE: BH) — $374.19, down 0.95 percent, 52-week low/high ($258.92 - $464.77).

• CC Media Holdings (Pink Sheets: CCMO) — $6.50, up 8.33 percent, 52-week low/high ($5 - $11).

• Cullen/Frost Bankers Inc. (NYSE: CFR) — $55.36, up 0.38 percent, 52-week low/high ($50.04 - $62.59).

• GlobalSCAPE Inc. (AMEX: GSB) — $2, up 1.01 percent, 52-week low/high ($1.78 - $3.14).

• Harte-Hanks Inc. (NYSE: HHS) — $7.91, up 0.38 percent, 52-week low/high ($7.59 - $13.74).

• Kinetic Concepts Inc. (NYSE: KCI) — $56.24, up 0.92 percent, 52-week low/high ($31.84 - $59.71).

• NuStar Energy LP (NYSE: NS) — $63.29, up 0.97 percent, 52-week low/high ($55 - $71.69).

• NuStar GP Holdings LLC’s (NYSE: NSH) — $35.03, up 1.39 percent, 52-week low/high ($26.73 - $39.98).

• Pioneer Drilling Co. (AMEX: PDC) — $13.80, up 3.06 pe ...

If you want to buy a home..for yourself or for rental..now is the time and the Alamo City is the place. With five (5) bases here, Military City, U.S.A. will keep those rentals full due to the transitory nature of the Military. Lackland, Fort Sam and Randolph alone could accomplish that. But the sad fact remains that an unemployment rate of 7 - 8% may look good compared to other areas of the country...but has taken a toll here. Come and get 'em while the prices are low. 40K to 80K homes sit empty waiting to be snapped up. And these are decent, well cared for houses.

As for REITS, I've threaded the needle and will come out looking "better than I ought to be" threading the needle with CYS, IVR and AGNC.