must01 Chuck Carnevale 长尾巴毛之殇

http://seekingalpha.com/article/230856-why-buy-and-hold-will-always-be-a-sound-investing-strategy

http://blog.directededge.com/2009/02/27/on-building-a-stupidly-fast-graph-database/

Search Results

F.A.S.T.graphs™

https://www.fastgraphs.com/ - CachedFundamental Research

blog.fastgraphs.com/ - Cached

It seems like the debate regarding the merits of the "buy-and-hold" investing strategy is alive and well. We always find these discussions amusing, because we believe that it is such a pointless discussion. There is no general argument or case that can be made to support the buy-and-hold strategy or to negate it.

The only true answer to the buy-and-hold argument is it depends on what and/or when you buy-and-hold. If you buy the right company at the right price, then buy-and-hold is a great strategy. If you buy the wrong company at any price, then the buy-and-hold strategy is a dumb move. Also, if you buy the right company at the wrong price, then buy-and-hold would once again be a bad move.

General considerations

After the market crash of 2008 it seemed like buy-and-hold bashers came out of the woodwork. Everyone was pointing to the so-called lost decade to validate their thesis that buy-and-hold was a dumb move. In this era of day trading mania where investors are more inclined to own a common stock for mere minutes rather than years, many pundits and investors alike jumped on the anti-buy-and-hold bandwagon.

One critical point that we want to make early is that buy-and-hold is an investing strategy. Investing strategies by definition imply a long holding period. Speculation, on the other hand, implies shorter time frames where the speculator is attempting to exploit an arbitrage situation. Our point is not to debate the virtues of one over the other, our desire is to point out that investing and speculating are not the same thing.

As an investing strategy, there is an old adage that supports the virtue of being a buy-and-hold investor: "a portfolio is like a bar of soap, the more you handle it the smaller it gets." The true investor is looking for a place where they can allocate their capital in order to receive an attractive return on their capital at appropriate levels of risk. The higher the return they attempt to achieve, the higher the risk they're willing to take, and vice versa.

Another general comment to be made about buy-and-hold as an investment strategy refers to investors who are looking to generate income from their investments. Income investors have the option of either fixed income, i.e., bonds, annuities and CDs, etc.; or income producing equities, i.e., real estate, dividend paying common stocks, etc. Of course, they can invest in these asset classes separately or in packages like mutual funds, MLPs, REITS or ETF's, etc. These investments need to be owned for long periods of time if any harvesting of interest or dividends is to occur.

The many faces of buy-and-hold

The remainder of this article will look at situations where buy-and-hold is a great strategy as well as situations where it's not. For the sake of efficiency we will present these discussions in graphic form through the lens of our F.A.S.T. Graphs™ research tool.

Overvaluation caused the lost decade

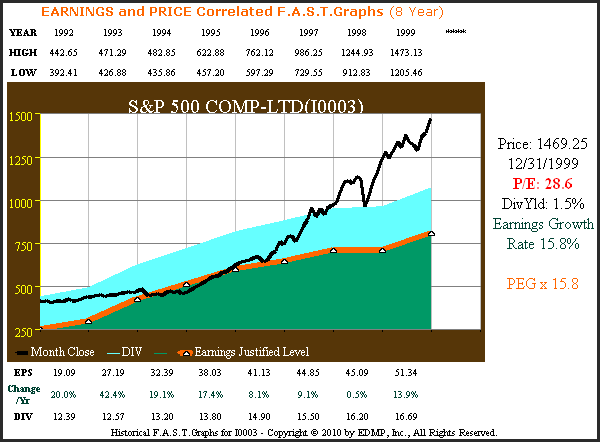

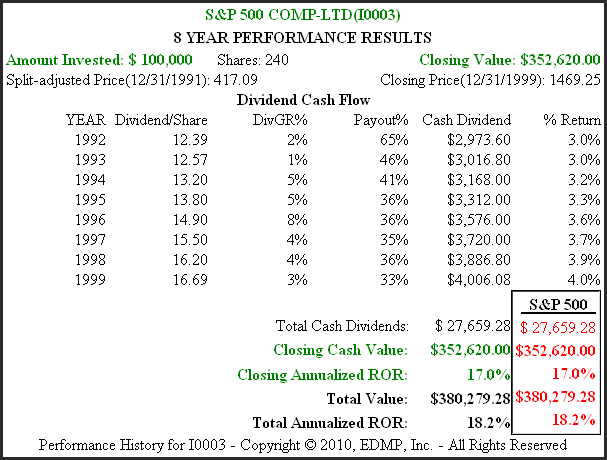

The following F.A.S.T. Graphs on the S&P 500 show the importance of valuation regarding a buy-and-hold strategy. The first set of graphs plots the S&P 500 stock price correlated to earnings for the period 1992 through 2009 and the corresponding performance over this timeframe. There are two important takeaways from these graphs: 1. Earnings growth for the S&P 500 over this time period was exceptionally high at 15.8%. 2. The year ending December 31, 1999, P/E ratio of 28.6 is close to double the historical normal S&P 500 P/E ratio of 15 indicating excessive overvaluation.

S&P 500 1992 to 1999 earnings to price

click to enlarge

S&P 500 1992 to 1999 performance

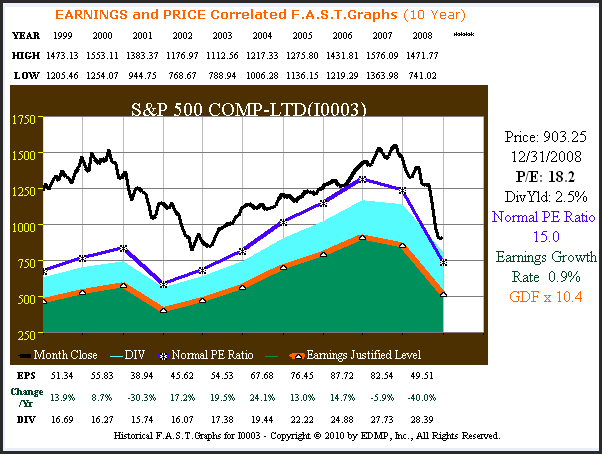

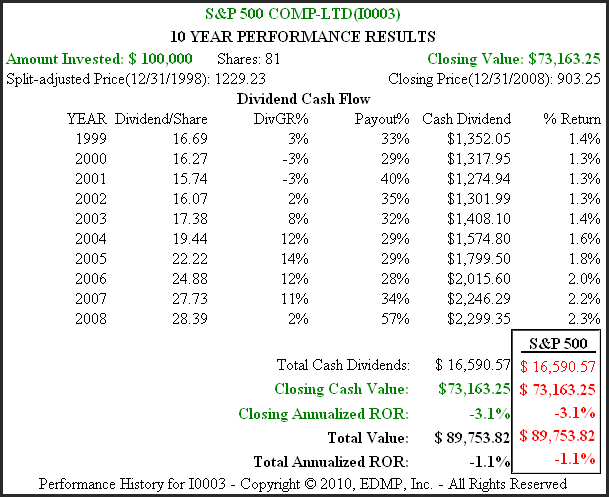

This next set of graphs on the S&P 500 covers the timeframe calendar year 1999 through 2008. These graphs cover the period most often referred to as the lost decade. Even though it includes the recessions of 2001 and the great recession of 2008, it is clear from this chart that overvaluation was the major cause of investor losses. Also note that earnings growth for the S&P had fallen to a historically low .9% per annum. We have added the normal 15 PE Ratio line (blue line with asterisk) to provide a clear perspective of the normal historical valuation for the S&P 500.

S&P 500 1999 to 2008 earnings to price

Overvaluation casued the lost decade

S&P 500 1999 to 2008 performance

From the above set of four graphs on the S&P 500 it is clear that buy-and-hold was an excellent strategy for owning the S&P 500 over the period 1992 to 1999. Notice that valuation was a little high at the beginning date and it was excessively high at the ending date. Also, earnings growth was abnormally high for this index. Therefore, it all added up to extraordinary returns for S&P 500 buy-and-hold investors.

In contrast, due to excessive overvaluation and poor operating results due to two recessions, the time period 1999 to 2008 was a horrible time to be a buy-and-hold investor. Note however, that overvaluation had more impact on shareholder losses than poor operating results. A lot of arguments either for or against buy-and-hold utilize measurements of performance based solely on stock price. We contend that measuring performance without simultaneously measuring valuation is a job half done.

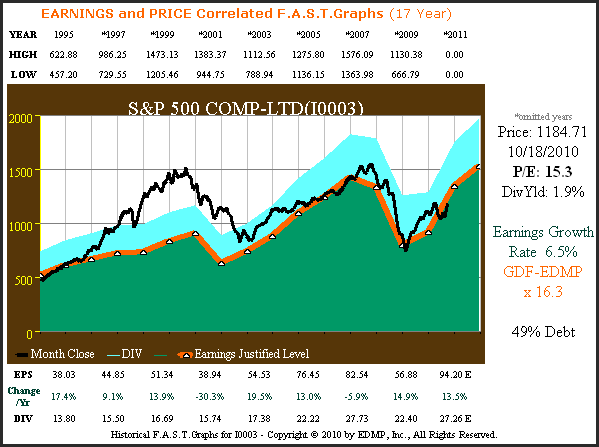

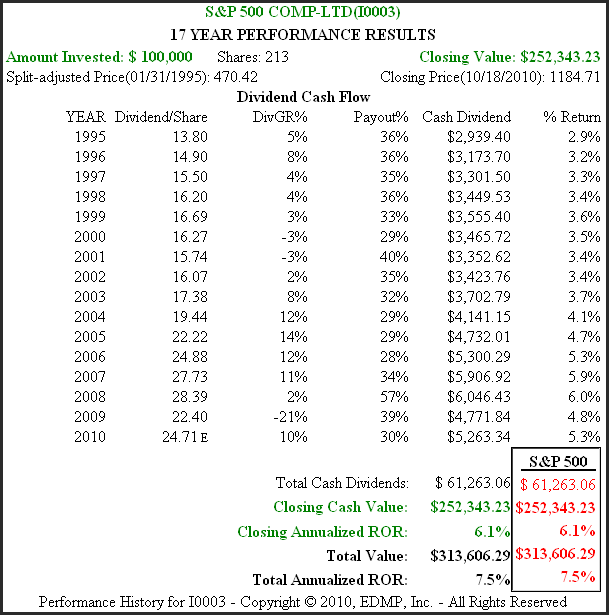

The S&P 500 is an important index and is often considered a proxy for the general market. The following graphs on the S&P 500 offer a look during a timeframe where both starting and ending valuation were normal at 15 times earnings. Over this 16 3/4 year time frame a lot occurred including, periods of significant overvaluation, two recessions, etc. Yet, what is crystal clear is that long-term performance not only correlated closely to earnings, but is also clearly a function of earnings as long as valuation is sensible. Therefore, the closing annualized ROR of 6.1% correlates very closely to the earnings growth rate of 6.5%.

S&P 500 17yr. earnings to price

S&P 500 17yr. performance

Over the calendar year 1995 to current timeframe, owners of the S&P 500 when purchased at True Worth™ value and held until today, where True Worth™ value once again is manifest, received returns that were consistent with operating results. If you are going to be a buy-and-hold investor, it is imperative that the principles of valuation as they relate to earnings (operating results) is understood, respected and investment buy/sell decisions are properly executed accordingly.

When growth and value are aligned

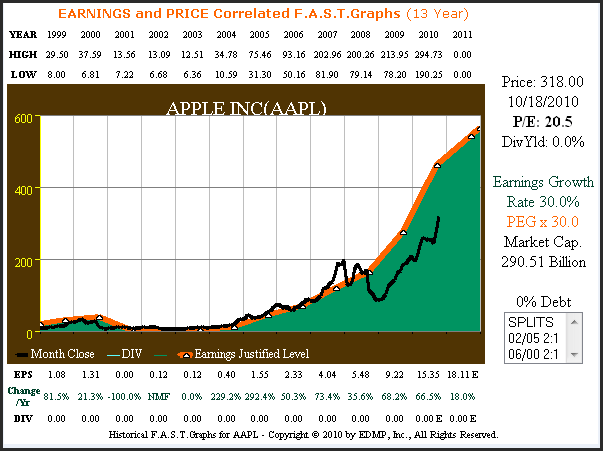

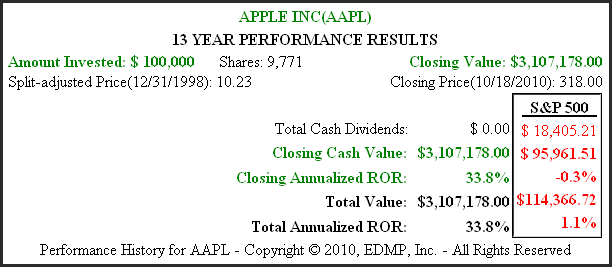

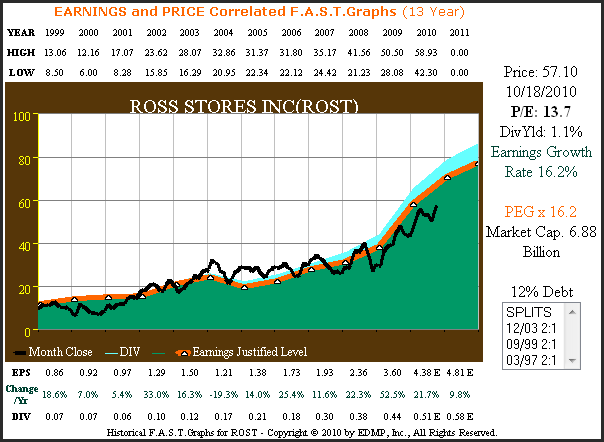

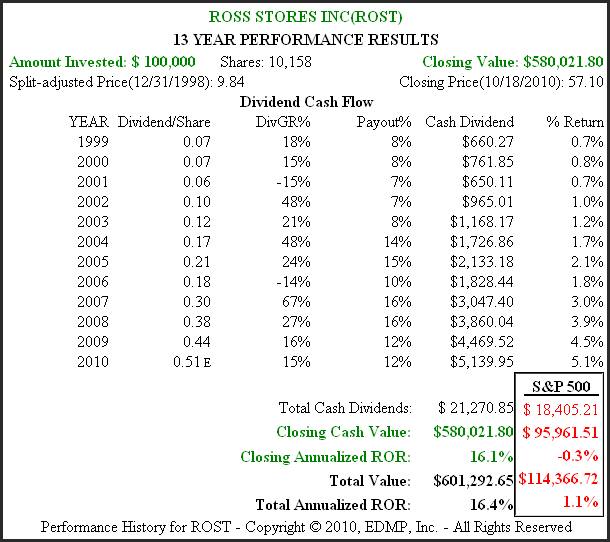

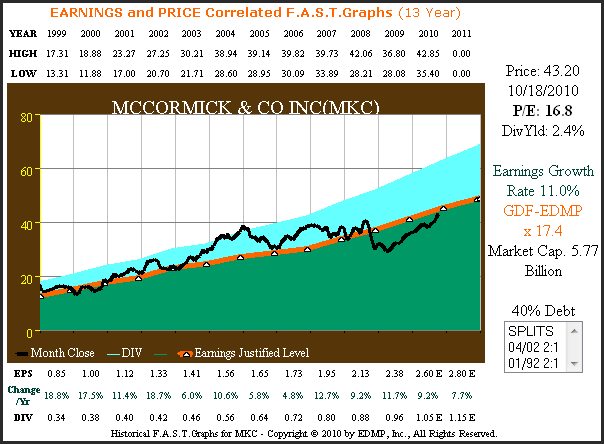

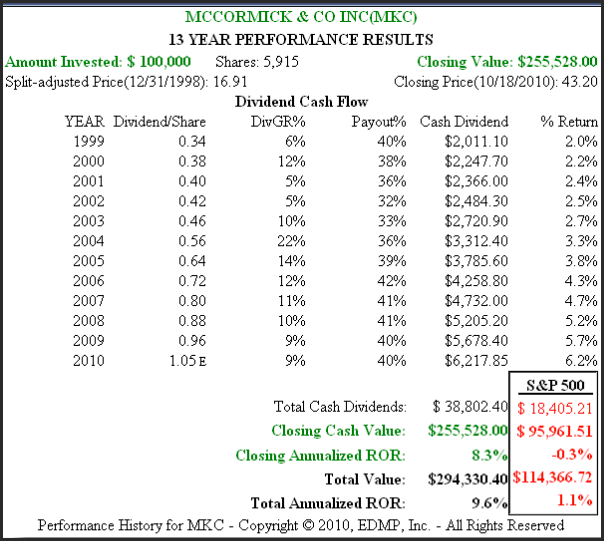

The next series of graphs portrays three companies over the timeframe 1999 to current, that illustrate how effective a strategy buy-and-hold can be. At varying degrees, each of these companies possess extremely consistent and strong earnings growth, and each was reasonably valued at the beginning date of this time period. Our first choice, Apple Inc. (AAPL), provides an example of a pure growth stock. Our second choice, Ross Stores (ROST), provides an example of a growth stock with a dividend component. Our third and final choice, McCormick & Co. (MKC), provides an example of a dividend aristocrat growth and income stock.

Each of these examples provide undeniable evidence that a buy-and-hold investing strategy works extremely well when the right companies are originally purchased at the right valuations. We see this as compelling evidence that the buy-and-hold strategy, done right, is a great and prudent way for people to invest.

AAPL 13yr. Earnings & Price Correlated

AAPL 13yr. Performance

ROST 13yr. Earnings & Price Correlated

ROST 13yr. Performance

MKC 13yr. Earnings & Price Correlated

MKC 13yr. Performance

When buy-and-hold is a dumb move

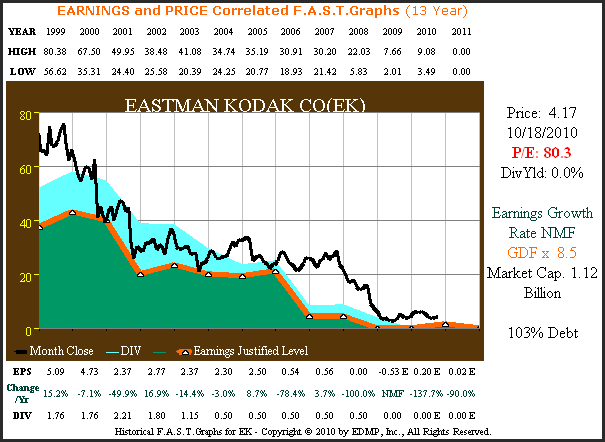

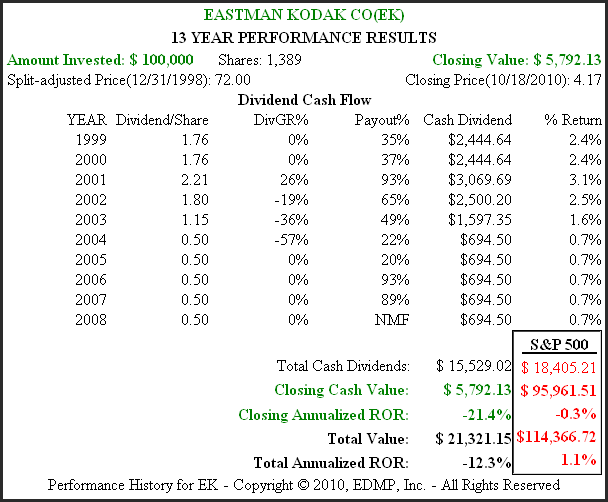

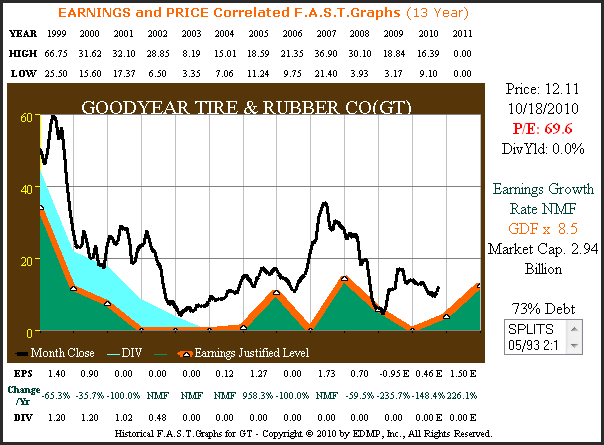

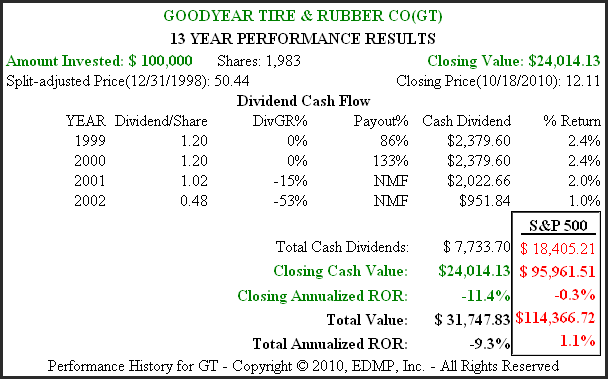

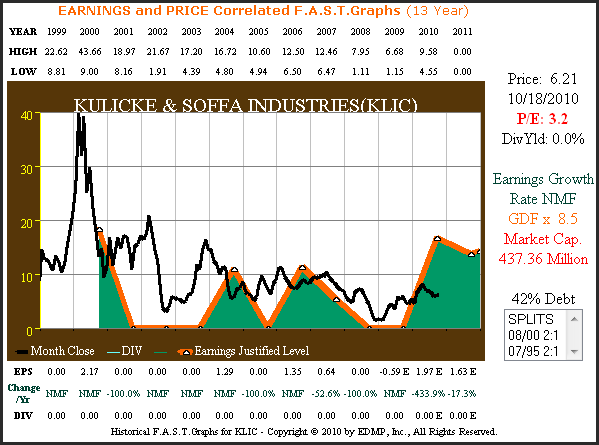

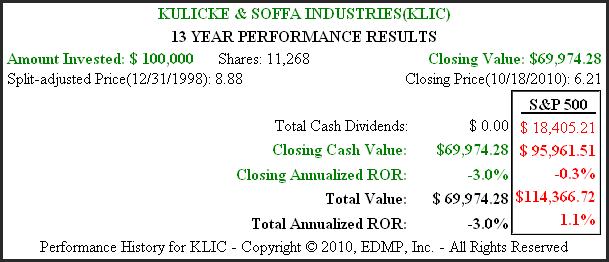

The next series of graphs portrays three companies over the timeframe 1999 to current that illustrate when buy-and-hold is a dumb move. Valuation does not really apply in these examples as it all comes down to terrible operating results. We will let the graphs speak for themselves and as you will see that collapsing earnings and/or very cyclical earnings growth does not work with a buy-and-hold approach. Why would anyone have wanted to buy-and-hold these three companies since calendar year 1999? The question is rhetorical because the answer is so obvious.

EK 13yr. Earnings & Price Correlated

EK 13yr. Performance

GT 13yr. Earnings & Price Correlated

GT 13yr. Performance

KLIC 13yr. Earnings & Price Correlated

KLIC 13yr. Performance

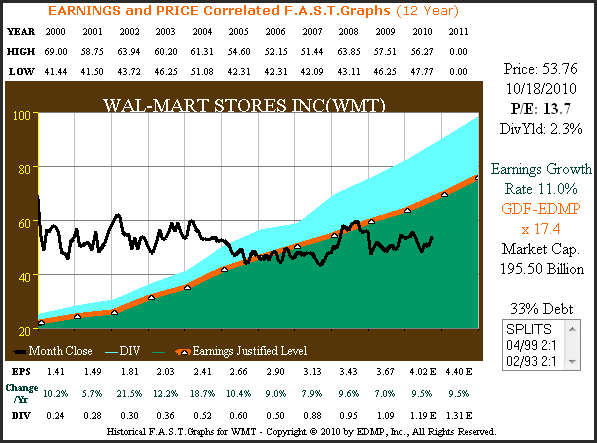

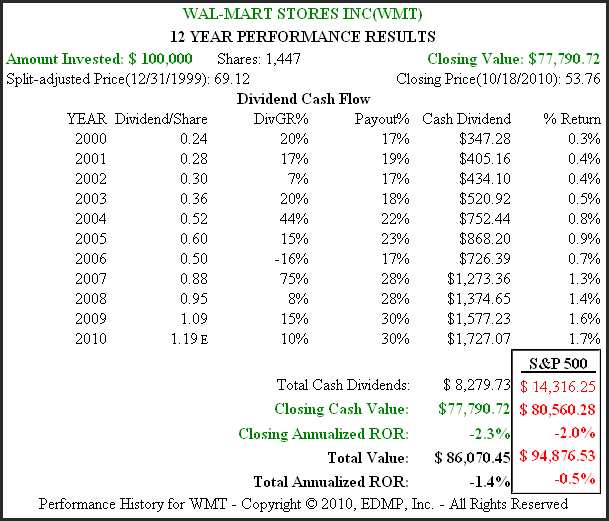

Even the best can be dangerously overvalued

This next series of graphs illustrates how overvaluation can destroy buy-and-hold returns for even the best of companies. Our first example looks at Wal-Mart (WMT) since calendar year 1999, and is one that we've written about before. At the beginning of calendar year 2000, Wal-Mart was trading at over $69 a share while True Worth™ valuation was indicated at approximately $22 a share.

While many overvalued stocks experienced a severe and rather immediate correction in calendar year 2000, Wal-Mart’s stock price went sideways for the better part of seven years before aligning with True Worth™ valuation. Perhaps buy-and-hold Wal-Mart investors were simply unwilling to sell this great business. But notice that even though earnings growth equaled a very consistent 11%, long-term buy-and-hold shareholders lost money over this timeframe because of beginning overvaluation.

WMT 12yr. Earnings & Price Correlated

WMT 12yr. Performance

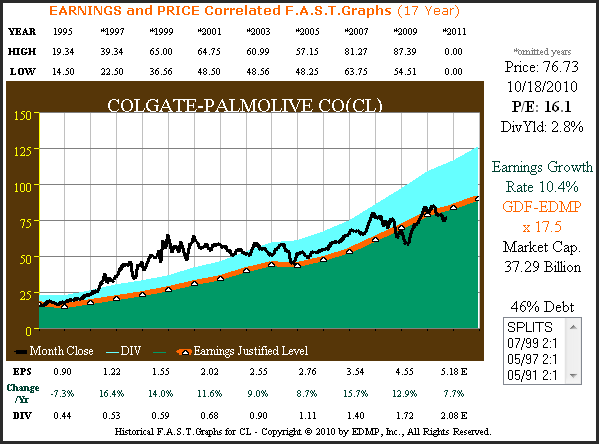

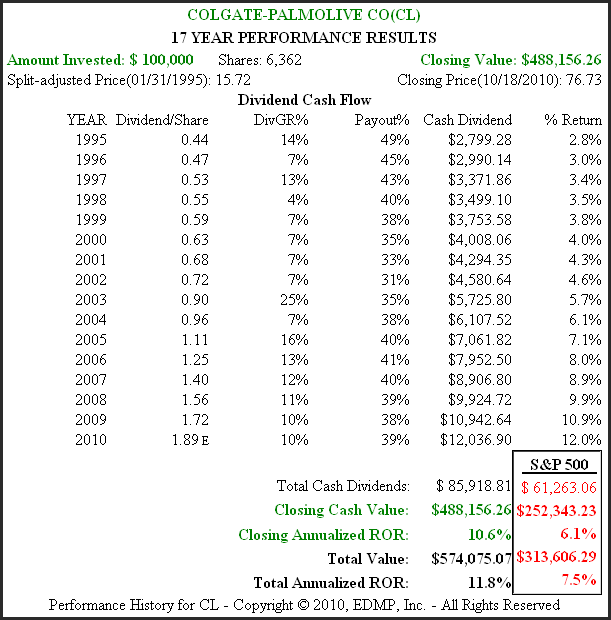

Our next example that illustrates the pitfalls of overvaluation looks at Colgate-Palmolive (CL). Our first graph looks at this blue-chip dividend paying stalwart for the period calendar year 1995 to current that correlates to our S&P 500 example above. As you can see from calendar year 1995 to calendar year 1999, Colgate-Palmolive’s stock price became increasingly more overvalued as it disconnected from its earnings justified valuation (orange line with white triangles). Like Wal-Mart, but not as extreme, Colgate’s stock price went sideways until October of 2004 until once again it touched its True Worth™ valuation line.

CL 17yr. Earnings & Price Correlated

CL 17yr. Performance

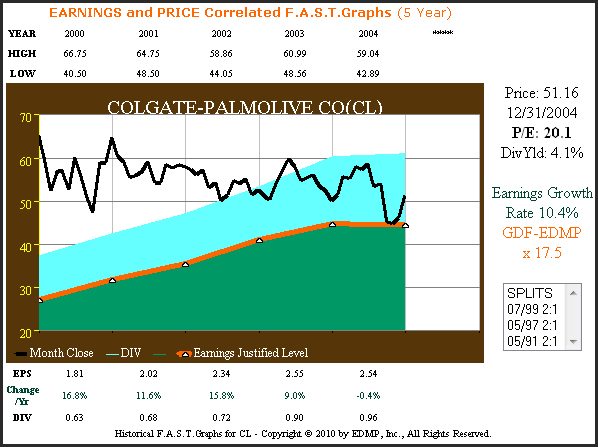

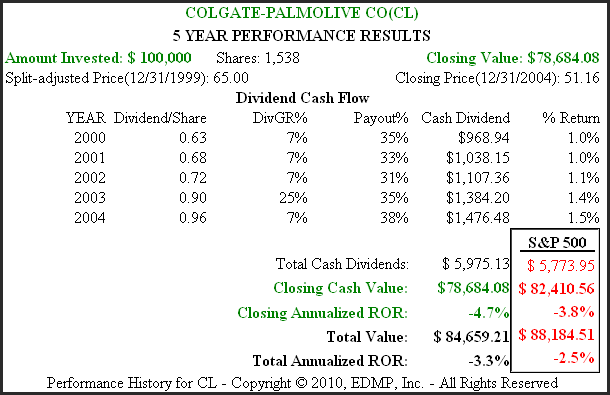

The following set of graphs review Colgate just for the overvaluation period, Calendar year 2000 through calendar year 2004. Clearly, calendar years 2000 to 2004 were not an attractive buy-and-hold timeframe for Colgate shareholders.

There are two interesting things to note on the price and earnings correlated graph. First, note how high Colgate’s stock price was relative to True Worth™ valuation at the beginning of calendar year 2000 which caused it to go sideways, not withstanding short bouts of volatility. Next, note how a modest drop in earnings in calendar year 2004 provided the catalyst to bring their stock price swiftly down into True Worth™ value.

CL 2000 to 2004 earnings to price

CL 2000 to 2004 performance

Conclusions

The main premise behind this article was to illustrate how the general arguments regarding whether buy-and-hold is a good strategy or not are frankly ridiculous. The validity of buy-and-hold as a sound investing strategy is predicated on many factors. Some of the primary ones, are what you buy-and-hold and the price at which you buy-and-hold it at. As the examples above illustrate, you can't just buy-and-hold anything, furthermore, you can't just buy it at any price either. For buy-and-hold to truly be an effective strategy, it has to be done right. However, when done right it is a terrific way for people to invest their capital.

A secondary premise behind this article was to illustrate the profound and fundamental difference between true investing and speculating. Buy-and-hold is an investing strategy that implies the appropriate holding time period, which is a hallmark of any strategy called investing. Speculation on the other hand is usually associated with shorter time frames where some element of arbitrage is applied. Whether speculators will admit it or not, there is more risk associated with this tactic than there is with sound fundamental investing practices like buy-and-hold.

At the end of the day, the practical application of a well thought-out and disciplined buy-and-hold strategy has proven itself and really needs no defense. In the long run buy-and-hold will be more tax efficient and less costly than more active strategies. This is not to say that more active strategies can't be profitable, it simply means that they're more difficult, costly and riskier to execute effectively.

Disclosure: LONG: AAPL, ROST, MKC at the time of writing. The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

长尾巴毛之殇

2011-01-28 09:10:27 来源: 网易科技报道 跟贴 0 条 手机看新闻国内长尾企业分几类,一种是百度谷歌,一种是中移动为首的国企,第三种是社会。

网易科技专栏作者 郭建龙

“如果说互联网行业是一条巨大的长尾,那么我只不过是长尾上的一根毛,现在毛快被剃光了,一条秃尾巴再长又能做什么?”

前两周,我突然接到一位陌生朋友的电话。几年前,我曾经做过一篇百度的调查稿,为了寻找线索,在网络上找到一位做百度竞价人员的电话,在保证不泄露他身份的情况下,请他谈了谈百度代理方的情况。

稿子做完,我就把这人忘记了。然而他却记住了我的联系方式,最近又看到了我在网易的专栏,决定在“从良”时,联系我将这几年的苦水倒一倒(并非针对百度,而是他从事过的N种IT工作)。所谓从良,是指从互联网行业中退出,加入了当地的联通,成了一位临时工。

在谈话时,他毫不客气地尽情讽刺着自己,说曾经认为自己有经商的能力,能够成为狮子,后来却发现只不过是长尾上的一根尾巴毛,到如今,连毛也不是了。

我甚至连他的名字都不知道(上次采访后忘记了,这次他不肯说,我不妨叫他张三),但感觉他的经历虽然普通,却很有代表性,几乎每一个在基层打拼的网络人都会遇到类似的问题。因此征得他的同意,将他的经历写出来,或许能够引起我们的思考,理解一下长尾巴毛们的生存状况。

三根尾巴毛的故事

张三没有上过大学,十七八岁就来北京混过,在某二流网站做过事,由此学会了网页设计技术。后来该网站逐渐没落,他决定回家乡闯荡,离开了北京。

在老家,他卖过电脑,帮企业做过网站,也做过百度代理。

显然,他熟知安德森的长尾理论,因此嘴巴里总是挂着尾巴毛这几个字,给我留下了深刻的印象。他形容他前期的经历相当于依附了三条尾巴。

先是作为联想(可能还做过其他牌子,我没有时间细问)的小代理商,之所以联想也被称为“一条长尾巴”,是因为联想电脑产业链的神经末梢是一个个的代理商,除了大的商家之外,联想之所以能够在中国打败其他电脑厂商,依靠的是庞大的销售网络,每一个网络末端就是一个小代理商。每一个小代理出的货都是有限的,轻得像根尾巴毛,但是把他们的销售量加起来就十分可观了。这样说来,的确还符合长尾理论的定义。

他还参加过当地的联想分公司组织的代理商大会,脖子上挂着塑料标牌坐在几百人的中间,仿佛找到了组织。由于我也见过类似的大会,因此非常理解他的归宿感。

但是,他最后却不得不换了尾巴,原因是电脑生意并不好做,他做电脑的朋友中有的人发了小财,但没有人能够发大财。虽然目前家庭电脑需求量很大,但一是城市太小,商家太多,二是工商税务和城管们仿佛根据他们的收入流来课税,收入多了就多收税,少了就缓一缓免得死掉,一句话决不让他们有太多的钱。到最后,由于入行太晚,他的生意没有铺开,于是离开了电脑销售行业。

他转战到了一个相关的行业:帮企业做网站。其实这个活儿在他卖电脑时就在做了,当时是兼职的,后来发现这个生意很惬意,虽然价格不一,但碰巧时,竟然一个网站也能挣一两万。平均下来,一年做十几个网站就不愁吃穿,比卖电脑轻松多了。更重要的是,做网站赚的钱是不用交税的,省去了工商税务的盘剥。

他的客户甚至还包括两个政府部门,其手续是这样的:政府部门将网站包给当地的关系企业,关系企业再把网站包给他。他不知道关系企业收了政府多少钱,但他给事业单位做的两个网站收入都在一万以上,至于给其他人或单位做,也就是几千元,有的甚至只有几百元。

然而,好景不长,这样的惬意只维持了一年多,当张三把熟人和熟人的熟人的网站做完了,客户就不够了。这时当地的一位百度代理商找到了他。

百度代理商除了卖百度关键字,一般还附加一个服务:做网站。比如,他们向一名跑运输的人拉广告,告诉他,如果使用百度竞价排名,业务会立马提升,车轮会忙得停不下来。对方将信将疑,但提出了最大的问题:“我还没有网站嘞。”代理商就会说:“我帮你做一个。”这样的网站通常只有几个页面而已,最重要的不过是一个电话,其他的只需要随便排一下版,不显得太乱就行。

这样的网站从几百到上千元不等,比起当初帮政府做是差远了。但毕竟是个事情。他不算该代理公司的正式员工,但隔三差五会分一些网站来做。

这时的他又开始兼营百度关键字,自己拉客户了,成了一名黑代理。所谓黑代理,就是没有经过百度授权,但由于百度账户的注册是开放的,任何人都可以注册。因此,他做的工作就是代替客户注册和选择关键字,并帮助客户进行维护。

与联想一样,百度成功的关键除了所谓的商业模式外,更在于一个全国性营销网络,你走到任何一个地方,都可以找到百度的代理。这些代理有的经过授权,有的没有经过授权,也就是黑代理。正是这些人帮助百度打下了江山,让百度的股价成十倍地增长。但这些黑代理们也只不过是尾巴毛,为了生存而已。

这次,好景又不长。百度经过了一系列事件后,开始收紧对代理商的要求,而最先受到打击的是最末节的张三。加上代理公司知道他在私底下接活之后,派人来警告他不要抢生意。于是他又从百度的长尾巴上出局了。

第四根

一个歪打正着的动作却给了他新的机会。

在做百度代理的时候,张三自己做了一个小网站,算是一扇宣传自己的窗口。为了吸引访问量,他在网站上建了个下载区,又建立了一个BBS社区,除了讨论一些技术、关键字广告之外,还开设了几个分坛讨论当地的生活、饮食,再加上几个半遮半掩的美女图片论坛。后来小游戏火了之后,又挂上了小游戏。

经过一段时间,该网站竟然在当地有了点儿小名气,人们讨论本地事情时喜欢上这个论坛,加上不停有人询问哪里有馆子、猫狗医院等等信息,依靠口口相传的力量,拉来了不小的流量。

张三适时地在网站上加入了google的广告,他没有透露收入情况,但从语气来看,应该可以维持生活。

他的父母容忍了他不上班的现实,以为他在网络上创业。

如果说整个互联网是条长尾巴,那么张三就是整个互联网的尾巴毛。如果再细分,他依靠康盛创想的Discuz!和UC Home免费软件搭建论坛,成为了康盛创想产业链的一份子,同时利用google广告赚钱,成了google超长产业链的一份子。

但这时,麻烦来到了,张三发现自己进入了一个不受鼓励的行业。

最初,有人出于好意来提醒他,他的网站过于热闹了。热闹,是每个从业者最愿意看到的局面,却是每个管理者最不愿看到的局面。

一位曾经的金融主管告诉我,管理者有千万个理由对行业进行管制,但真正的原因只有两个:一是方便管理,二是利益。对于互联网,这样的说法同样成立。

张三没有把这样的好意当回事儿,于是,正规的机构出场了,告诉他,由于缺乏备案,他的网站实际上是非法运营的。

作为应对,张三把网站挂到了一位朋友的公司,希望规避监管风险。

但这时,家庭的阻力来到了。他的父母以为儿子在创业,却没有想到创业原来这么有风险,和监管者对着干的一定不会有好下场。

在监管者和父母的集体施压下,张三终于认识到,在国内,不管你做哪一种尾巴毛,结局都是慢慢憋死。加上由于要结婚,女方父母要求他有个正式的工作,他终于幡然悔悟,决定关闭网站,加入了当地的联通,成为了“共和国长子”中的一份子。虽然属于临时工,但在女方父母看来,联通这个牌子就说明这是个不错的工作。

但张三的反骨真的消失了吗?作为最后一次释放,他找到了我,悲愤地说出了篇首的那句话。也许说完之后真的老实了,但我不敢肯定。

几种长尾巴

张三认为,国内的长尾企业分成几类。

一种是像百度、google这样的民营巨头。如果让我加,我还会加上更为典型的淘宝,但张三由于和淘宝没有接触,没有谈。

另一种是中国移动为首的国企。

第三种是社会,这才是最大的长尾。

第一种不用详谈,但张三认为,在国内有一个很大的特点,长尾企业总是拿尾巴开刀。以百度为例,依靠各种各样的广告客户,加上勤奋的代理商,百度发了大财,但一旦代理商打下了天下,百度开始自己做业务,回收代理权。这样做的还包括google。至于客户,百度也一直在涨价,以至于曾经有客户咆哮着跑来找他控诉,让他感到头皮发麻。

我认为,淘宝最近的案例也可以算一个。一旦小卖家为淘宝赢得了未来,淘宝就开始变脸。

当然,这和网站天然的限制有关,入口太少,卖家太多。但也和监管有关,严格的监管迫使淘宝不得不像个城管一样对待小卖家,结果,尾巴毛被越拔越少。把自己的尾巴毛在外界看来是疯狂的举动,但在严格的监管下,一切都是可能的。

另外,我还认为,国内有一个非常可惜的长尾案例,就是康盛创想。如果说国内哪些企业对中国互联网的贡献最大,我想,康盛创想即便不是第一,也绝不比其他巨头差。康盛创想做出了国内最优秀的软件,供全国大大小小上百万网站使用,然而这些尾巴毛却为康盛创想带不来太多收入,并且随着张三这样尾巴毛的死去,康盛创想的尾巴变秃了不少,令人扼腕。

张三之所以把中国移动也称为长尾,是指中国移动雁过拔毛的特征,拥有超强的收费能力,又养着一个不小的寄生集团。

然而中国移动也不得不拔自己的尾巴毛。一是出于自愿,如同最初中移动整治sp之时一样,当sp发展到一定程度,中移动发现它很赚钱的时候,就决定自己做,于是sp死光了。

二是出于领导想当官的压力。如今新领导上台后所谓的新政就是如此。

但张三最精彩的观点是,整个社会也是一个巨大的长尾。但我们的社会到底怎么拉?严苛的法律使人们胆战心惊,且不纯粹是法律,还有各种各样非法律的压力。税收机关则虎视眈眈盯着任何一个可能的税源,不管是海关的关税,还是网商。到处充满了拔毛者,那么尾巴能不秃吗?

我记得一位老人说过这样的一句话:监管者最需要注意的是,要让被监管者在合法的范围内能够得到足够的利润,如果做不到,那么出问题的绝不是被监管者,而是监管者和法律本身!

WENXUECITY.COM does not represent or guarantee the truthfulness, accuracy, or reliability of any of communications posted by other users.

Copyright ©1998-2026 wenxuecity.com All rights reserved. Privacy Statement & Terms of Use & User Privacy Protection Policy