hulao2015不懂乱踩没道理。pigtiger1973只不过分享自己的经验,自己在其中是不占什么好处的,最多就是从平台拿一点referal reward(必须自己是member才能介绍)。

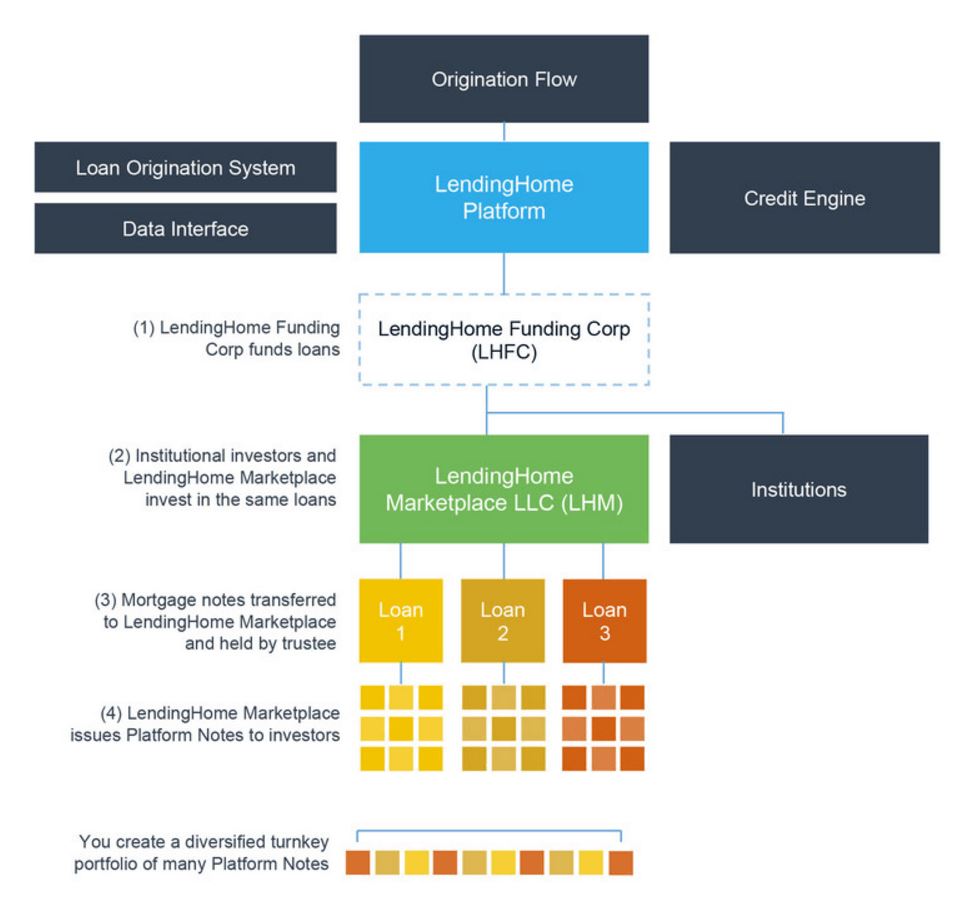

以LendingHome为例看一下它的众筹平台结构:

其中LHM (LendingHome Marketplace LLC) 就是所谓bankrupcy repote entity。即使LendingHome Platform破产,LHM还能继续活下去,换一家公司继续 serve mortgate payment cash flow,让钱流向mortgage payment dependent note investor。

LendingHome怎么赚钱呢?一是mortgage loan origination fee (borrower pays),二是charge invester 10% of the gross interest payment (比如gross interest rate是10%,到invertor手上net interest就只有9%)。

Borrower default怎么办呢?那些lien是在某个trustee手里,归LHM管理,可以forclose卖掉抵押的房地产。如卖掉所得的钱扣去各种费用不够还利息、本金,那investor就可能有利息甚至本金的损失。

这家平台的note有多少delinquent or default? 据该平台自己介绍:

"Our portfolio currently includes over 5,300 loans of which 5.78% have ever hit the 120+ day delinquency stage. Once a borrower is 30 days late on their monthly payment or their maturity date, we consider that loan to be default, and our in-house servicing team works closely with borrowers to bring them back to current. Delinquent loans may, but do not necessarily, produce a loss. Of 39 foreclosures and 12 short sales to date, only two resulted in a loss of principal.

Roughly 87% of LendingHome’s active servicing portfolio is current as of 12/31/2016."

我补充一下自己的看法。投资这类有抵押的债务LTV当然很重要,但另一个容易被忽略的因素是loan size。如果loan size太小,遇到default那些fixed cost很容易就超过LTV的缓冲。如果loan size太大,underlying房地产可能不容易脱手。