因为牛经沧海曾经有过专业的市场投资经历,所以对于他的提示,我去查找阅读了一些相关资料,也做了一些思考。

美国市场的REIT的历史很长,具体种类也很多。90s REIT 的发展变化是蛮大的,特别是法律监管的修改。

在1985 -1990, US Mortgage based 的REIT占市场比重从45%降到20%, 目前是6%,之前网友提到的NLY, AGNC, CIM都属于这一类。在过去二十年,主力REIT是EQUITY BASED, 目前市场比重94%。 加国市场基本是后者。

1991年,美国REIT市值130亿规模,2016年9320亿规模,市场规模增长70倍。

从行业整体而言,今日的REIT与90s初期已经发生本质变化,目前EQUITY BASED的REIT的金融杠杆较低,即使利率变化,对其影响也远不如90s。

利率对所有投资资产的估值影响是基本等同的,REIT所面临的利率变化风险并不明显高出其它投资类型。

( 福布斯文章,仅供参考。Why 2016 Should Be An Awesome Year To Invest In REITs)

(我在加股REIT下跌30-50%时,特别推荐投资加国REIT,我并不推荐在目前价位投资美加市场REIT。)

“Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble”

“Long ago, Ben Graham taught me that ‘Price is what you pay; value is what you get.’ Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.”

Leverage and Coverage Ratios

(Balance sheet data as of Q4 2015)

Equity REITs

- Debt Ratio: 33.4%

- Coverage Ratio: 4.1x

- Fixed Charge Ratio: 3.7x

- 46 Equity REITs are rated investment grade, 68 percent by equity market capitalization.

All REITs

- Debt Ratio: 43.6%

- Coverage Ratio: 3.8x

- Fixed Charge Ratio: 3.5x

- 46 REITs are rated investment grade, 62 percent by equity market capitalization.

- Coverage ratio equals

EBITDA divided by interest expense. - Fixed charge ratio equals EBITDA divided by interest expense plus preferred dividends.

Early 1990s recession

The recession of the early 1990s describes the period of economic downturn affecting much of the world in the late 1980s and early 1990s. The global recession came swiftly after the Black Monday of October 1987, resulting from a stock collapse of unprecedented size which saw the Dow Jones Industrial Average fall by 22.6%. This collapse, larger than the stock market crash of 1929, was handled effectively by the global economy, and the stock market began to quickly recover. However, in North America, the lumbering savings and loans industry was facing decline which eventually led to a savings and loan crisis which compromised the wellbeing of millions of Americans. The following recession thus impacted the many countries closely linked to the United States.

Real Estate Downturn of the Early ’90s Differs From Today’s Crash In Important Ways

David J. Lynn, Ph.D. Nov 2, 2009

Many market observers have pointed out similarities between the current downturn in commercial real estate and the downturn in the early 1990s. Both were preceded by an extended period of relaxed underwriting standards, excess capital chasing returns, significant cap rate compression, and steep increases in asset values. It is useful to compare and contrast key elements of the two periods in order to establish a reference point for today’s investment strategies.

Two key regulatory changes during the 1980s paved the way for the overbuilding that defined the 1990s recession in commercial real estate. The 1982 tax cuts included provisions that allowed for generous depreciation allowances and tax shelters for investors. Also during the 1980s, the deregulation of the savings and loan industry allowed these institutions to expand their investments to include commercial mortgages.

The tax laws were changed again in 1986 to remove many of the earlier incentives for real estate investment. But the combination of a general atmosphere of economic recovery, an increasing appetite for real estate investment from institutional capital, and the introduction of the S&Ls as new and often inexperienced lenders for commercial real estate resulted in a massive oversupply of space in many markets.

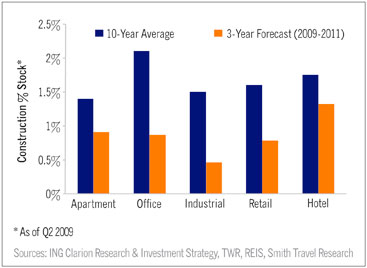

The silver lining in today’s environment is a general lack of oversupply in most markets. New construction in nearly every sector has been below long-term trends, though some markets are struggling with oversupply problems [Figure 1]. While ample financing was made available for development projects in recent years, the combination of supply constraints and sharply rising land and construction costs helped to keep new supply largely in check.

The primary problem for commercial real estate today is a lack of demand, caused by an economic recession that includes significant job losses, a historic decline in consumer spending, a global slowdown in import and export activity, and the collapse of the residential housing market.

The recession is reaching all property types, and vacancy rates are expected to approach or surpass 20-year highs. The lack of financing for new construction will likely keep new supply further constrained for some time, helping to improve real estate fundamentals as the economy recovers over the next few years.

FIGURE 1: NEW SUPPLY REMAINS IN CHECK COMPARED TO HISTORIC RATES

Dealing with distressed assets

The collapse of the commercial real estate market in the 1990s led to the passage of the Financial Institutions Recovery, Reform and Enhancement Act (FIRREA) of 1989. That legislation, aimed at bailing out the savings-and-loan industry, established the Resolution Trust Corp. (RTC), which was charged with efficiently selling off the enormous quantity of bad commercial mortgages from failed financial institutions.

The RTC took over distressed assets from failing lenders and owners and facilitated a quick and painful write-down. The RTC forced the clearing of defaulted loans and helped to establish pricing, which allowed transaction activity to recover relatively soon after the market collapse. Once clearing prices were established, private capital moved in rather quickly, accelerating the bottoming-out process and eventual recovery.

In contrast, today there is little pressure from the government on the banks to mark their real estate portfolios to the market level. A series of plans and programs aimed at dealing with distressed assets — including the Troubled Asset Relief Program, Term Asset-Backed Securities Loan Facility, and the Public-Private Investment Program — have helped to avoid financial catastrophe. But these initiatives have had minimal impact in terms of actually addressing the distressed assets that were central to the financial crisis.

Most lenders are not willing to foreclose on troubled properties primarily because their balance sheets are already impaired to the extent that they generally lack sufficient capital to support significant write-downs. Some lenders and special servicers are playing “pretend and extend” as they extend loans to buy time rather than pursue foreclosures and take mark-to-market losses. As a result there have not been as many distressed transactions as market experts anticipated.

Complex capital stack

Real estate financing leading up to the 1990s recession was fairly simple. Life companies, pension funds and commercial banks provided the bulk of funding and held mortgages on their balance sheets that matched their long-term liabilities. In the wake of the 1990s collapse of commercial real estate, these traditional lenders pulled back sharply, focusing their capital on the refinancing of existing assets.

Eventually, new capital began to flow into the market to take advantage of distressed pricing, with valuations falling between 30% and 50%. Capital came from opportunistic investors and later from a revitalized REIT industry buoyed by tax reforms.

The same FIRREA law that established the RTC also helped pave the way for the development of the commercial mortgage-backed securities (CMBS) model, which revolutionized real estate finance. Because of the risk-adjusted capital requirements that FIRREA placed on financial institutions, they were encouraged to hold securitized assets rather than whole loans.

Bankers eventually modified the long-standing residential mortgage-backed securities (RMBS) model to apply it to commercial real estate assets, opening up another new financing source.

The demand for CMBS encouraged investment banks and conduit lenders to originate massive volumes of new loans. A new moral hazard in the model emerged because CMBS loans are not held on the originator’s balance sheet, causing reduced incentives for rigorous underwriting. Competition among lenders led to increasing loan-to-values and lower pricing, which helped fuel the sharp spike in real estate prices.

In addition, borrowers looking to minimize financing costs and equity contributions often supplemented senior mortgages with an increasingly complex array of subordinate financing, including mezzanine and preferred equity positions. The complexity of the new capital structures, especially for CMBS pools, has created a nightmare for workout situations.

In the last downturn, the workout mechanism was relatively simple, primarily involving a single lender and borrower. Today, the complicated capital stack makes sorting out the interests of the different players more complicated, time-consuming and expensive. With competing interests of the various tranches engaged in tranche warfare, it is even more challenging to form an agreement in the restructuring process.

Impact of institutional ownership

Over the past 15 years, commercial real estate has been increasingly accepted as a mainstream asset class by large pension funds and other financial institutions. The market value of the NCREIF Property Index — which tracks institutional investment in U.S. commercial real estate — surged by eight-fold, rising from $41 billion in 1994 to $328 billion in 2008.

While recent investments by institutions — particularly those at the top of the market in 2006-2007 — have likely suffered declines in value, they often have the financial capacity to support their investments through additional capital. In short, these institutions can help to extend or restructure debt to avoid foreclosure. We believe that this is another reason that we have seen relatively little in the way of distressed asset sales.

David Lynn is managing director and head of U.S. research and investment strategy with ING Clarion based in New York.

With more equity, REITs downsize risk in '90s

Today, real estate investment trusts (REITs) are respected by investors and real estate professionals as a sensible way to generate funds and create profits.

Now, REITs are more common and considered to be much less risky than their Disco-era counterparts. Back then, most REITs were focused on construction lending, and they were managed by outside advisers, typically banks.

Nearly 20 years later, most REITs are true operating companies that buy, develop, manage and sell real estate rather than make mortgage loans. They are often referred to as pass-through entities because most of the cash they generate flows to investors without taxation at the corporate level.

In 1979, most REITs in Atlanta and elsewhere were in the midst of a slump, having suffered for several years during a recession brought on, in part, by a pair of Arab oil embargoes, and the consequences of too many high-risk loans, said John E. Barron, an audit partner at the Atlanta office of Deloitte & Touche LLP and the firm's national director of REIT accounting services.

Many REITs were forced to liquidate their commercial real estate holdings, and some went bankrupt.

By about 1980, REIT activity began to revive and continued to gather steam during the decade. The Tax Relief Act of 1986, which authorized REITs to manage their properties directly, helped stimulate growth. So did a 1993 legislative change that eliminated REIT investment barriers to pension funds.

"Beginning around 1992 or 1993, there were a ton of new offerings," Barron said. There are more than 300 publicly traded REITs in the country, including at least 10 in Atlanta. The city also has several privately held REITs.

"REITs are some of the most active developers and owners in our city," said Thomas D. Senkbeil, vice chairman and chief investment officer of Weeks Corp., one of Atlanta's largest REITs.

Most of today's REITs are equity-based REITs, which invest in and own properties. About 87 percent of REITs fall into this category, and only 9 percent are mortgage-based REITs, the type that dominated the market 20 years ago. About 4 percent are a hybrid of the two.

Today's REITs may be more stable investment vehicles than those of the late 1970s. "REITs were probably more speculative then," Senkbeil said. Too many speculative loans on high-risk projects such as Florida condominiums were the downfall of many REITs, he added.

In their 1990s incarnation, REITs have a much more conservative capital structure, Barron said. They typically have roughly equal amounts of debt and equity, in contrast to the debt-heavy REITs of the past.

REITs today are also more safe and stable than those of the 1970s because they are internally managed, Barron said. Because the senior managers are usually also stockholders, the interests of the two groups are aligned. "There is much more incentive for management to perform well and not take too many risks," he said.

"Because we have a lot of discipline, you won't see the overbuilding and excesses of the past," Senkbeil said. Today's REITs also are more likely than their predecessors to diversify, with investments in different types of development (retail, residential, industrial and office) and properties in different parts of the country. This diversity lessens the likelihood of substantial losses if a particular market becomes overbuilt or a large project fails.

However, some of today's REITs still opt to specialize in one type of property or are active primarily in a local or regional market.

Weeks develops and manages suburban office and industrial properties throughout the Southeast and in Texas.

REITs make up about 5 to 8 percent of the commercial real estate market, with an estimated $125 billion in equity, Barron said. In contrast, the equity investment in REITs in 1979 was significantly lower, most likely between $1 billion and $5 billion, he estimated.

In one form or another, REITs have existed since the 1880s, when trusts were exempted from taxes at the corporate level if income was distributed to beneficiaries. This exemption was repealed in the 1930s but restored in 1960.

Like other stocks, REITs have experienced drops in the recent roller-coaster activity on Wall Street. Prices peaked in November 1997 and have dropped about 20 percent since, Barron said.

He predicted a recovery in REIT stocks during the next few years, although not necessarily a return to the previously high levels. As for Atlanta, which has been known as a high-growth market, REIT activity may slow somewhat as investors become wary of overbuilding. However, there will be an ongoing need for new residential and commercial development, Barron said, so REITs will probably continue to grow in the long run.